Restaurant toolkit

1min

1min

24 November 2025

As a restaurant owner, ensuring your guests have a positive dining experience is your top priority—yet profit margins are often anything but lavish. Between sourcing fresh ingredients and paying staff, every point of cost matters. Card processing fees might look small on paper, but those few percentage points can pile up quickly when you’re dealing with hundreds of transactions per day. In the UK, 80% of retail purchases are likely made via card or contactless payment, according to recent studies by the British Retail Consortium (British Retail Consortium).

It’s obvious your patrons expect the convenience of paying using cards or digital wallets. But as these forms of payment become ever more common, staying on top of what your provider charges—and whether you’re getting the best deal—can significantly impact your profitability. Deciding whether to switch providers can feel like a daunting task (who has the time to research new providers and renegotiate contracts?), but it can be a substantial money-saver. Think of it like upgrading your menu’s ingredients: when you switch to something better suited to your restaurant’s needs, everyone benefits.

Most UK restaurant owners aren’t thrilled to read the fine print on their monthly statements. With a bustling dining room to run, it’s easy to let small charges go unnoticed—until they’re not so small. Here are a few signals to watch for:

When any of these issues surface, it’s worth reviewing your service agreement. Much like tasting a dish that has just a bit too much salt, you can quickly sense that something isn’t right. Rather than swallow extra costs for another month, investigate a better solution.

Understanding where each pound goes can be the first step to determining whether you’re paying too much. Card processing fees can seem complicated, but let’s simplify them:

All these fees add up. In many UK restaurants, you might be paying anywhere between 1.5% and 3% of each card transaction. On busy days, that subtle percentage difference can translate into hundreds of pounds. Don’t let complexity stop you from saving money. Once you break down the components, it’s easier to spot if you’re paying for perks you don’t actually need—like advanced online payment features if you run a dine-in-only restaurant.

Meet Emma, the owner of The White Rabbit, a cosy, family-owned spot in Brighton, offering hearty vegetarian lasagne and fresh pastries. For years, she stuck with the same card payment provider, thinking the fees were “about normal.” Emma’s average monthly card volume was around £20,000, and her provider charged 2.5% per transaction. After doing her maths, she realised that was £500 slipping away in fees each month. On top of that, she had obscure additional costs for paper statements and an old payment terminal rental.

Curious if she could reduce these fees, Emma researched alternative providers and discovered competitive rates around 1.6% to 2%. In switching, she immediately saved over £180 each month. That’s more than enough to cover a few rounds of staff coffees, or occasionally invest in higher-quality produce for new seasonal recipes. But more importantly, her new payment system sped up checkout times, giving her staff extra minutes each day to focus on what they do best—serving delicious food.

An often-overlooked step is reviewing your current contract’s fine print. If you rush to sign a new deal without checking your existing agreement, you could face termination fees. While the notion of reading legal jargon can be about as appealing as peeling a mountain of onions, it’s a critical step. Look out for:

If your contract penalises you really harshly for leaving early, calculate whether the near-term penalties outweigh the long-term benefits. Sometimes waiting for your renewal date is the sensible path—especially if your contract ends in a few months. But if the cost saving is substantial and immediate, don’t let a one-time exit fee keep you from achieving better margins. As always, run the numbers thoroughly to see which move is best for your bottom line.

You wouldn’t select a supplier for your fresh produce without doing a bit of homework first. Similarly, you want to investigate potential payment providers. Remember: it’s not just about price, but also about reliability, customer service, scalability, and user-friendliness.

Ideally, you want a clear format for fees. Look for a provider that offers a straightforward breakdown: interchange, scheme fees, and provider markup. Make sure no surcharges pop up unexpectedly—like batch fees, statement fees, or monthly service “add-ons.” If their pricing structure is too convoluted (or if they’re reluctant to clarify details), consider it a potential red flag. This is your money; you deserve to know exactly where each penny goes.

Rolling monthly contracts are increasingly common, allowing you to leave with minimal fuss if you’re not satisfied. If a provider insists on a four-year contract and locked-in termination penalties, think carefully about whether the potential savings are worth the risk. Shorter contracts or flexible terms give your restaurant breathing room to pivot if your business model changes—like adding a takeaway service or pivoting toward more digital, contact-free payments.

Bad payment terminals or confusing checkout systems cost you more than a few pence in fees—they cost customer goodwill. Many modern providers offer sleek, user-friendly card machines and integrated apps that let your staff track tips, split bills, and reconcile end-of-day balances in a snap. Suppose you run a bistro with busy lunch service. Seamless, quick transactions mean faster table turnover, more happy customers, and less chaos for your team.

When your card reader malfunctions during the Friday dinner rush, you need a provider that’s immediately reachable. Whether it’s phone, live chat, or email, strong support can help you avoid losing sales or leaving hungry patrons frustrated. Research average resolution times—test out how quickly they respond to queries. After all, quality support might sometimes justify a slightly higher fee structure because every minute offline can cost your restaurant a small fortune.

Some providers quote their lowest possible transaction rate in giant font, but quietly slip in other charges. That’s like listing a cheap main course, only to discover the sides, the garnish, and even the seat cushion are extra. Here are some subtle charges worth double-checking:

These fees can quietly nibble away at your profits if you’re not vigilant. Make sure you know the full picture so you can budget correctly, or even factor it into your menu pricing. If you’re running a large, well-established brasserie, you might afford the occasional surprise fee. But if you’re a smaller eatery, every unexpected charge can sting.

If you’d prefer not to jump ship just yet, you always have the option to negotiate with your current provider. It’s easier if you can demonstrate your value—for instance, maybe you have a consistent track record, low chargeback rate, or an expanding business. Here’s how to approach that conversation:

Remember, negotiation isn’t just about cost—it’s about forging a partnership that empowers you to run your restaurant smoothly. If you succeed in lowering fees, great. If not, it might confirm that switching is the right choice.

Switching payment providers doesn’t have to be like changing an entire menu overnight. Yes, there may be new hardware, staff training, and a bit of paperwork, but you can often schedule these transitions at quiet periods—like early in the week or after-service hours. Here are some practical tips to ensure it all goes smoothly:

Once you do the groundwork, you’ll likely discover the switchover is not as scary as it first seemed. In fact, modern payment solutions tend to be quite intuitive, especially if they’re built to help smaller businesses succeed. It’s a bit like trying out a new recipe: do a test run, gather feedback, and then roll it out to your main menu confidently.

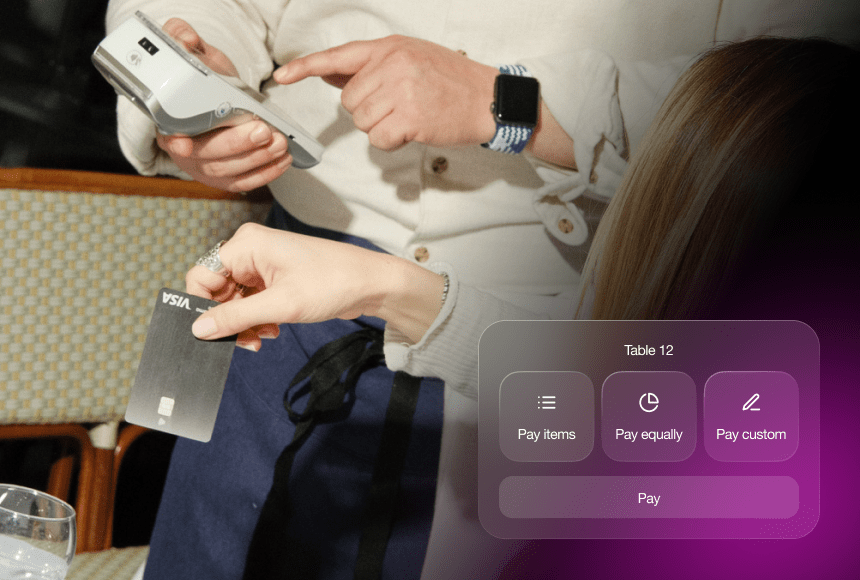

You might wonder: does a new payment provider have any direct effect on customer loyalty or repeat visits? You’d be surprised. Slow or cumbersome payment experiences can frustrate guests and reduce the likelihood they’ll come back. On the other hand, a speedy, seamless payment flow creates a positive final impression. That’s exactly where solutions such as sunday can play a role, allowing guests to scan a QR code, pay in seconds, add a tip, and even leave a review on Google if they’re so inclined.

A new or improved payment process becomes a subtle—and often underestimated—way of delighting patrons. You’ve worked hard to deliver a memorable meal; you don’t want a clunky payment experience to be the last thing they remember. Even in the UK, where the dining culture can vary greatly from region to region, an efficient, user-friendly payment experience is almost universally appreciated.

Beyond lowering fees, switching providers or upgrading technology can bring additional perks that boost your restaurant’s operation. Some advanced solutions integrate seamlessly with point-of-sale systems, enabling real-time reporting of sales, staff performance, and tipping patterns. You can even configure promotions or loyalty programs that automatically apply to certain menu items—saving you precious time and simplifying the admin side of running a restaurant.

Missing out on these functionalities can mean missing an opportunity to fine-tune your restaurant’s performance. Picture a kitchen that receives immediate alerts on orders, while front-of-house staff track the tables’ real-time status. As soon as a bill is requested, the system shows staff whether the table paid in the app or at the terminal. Suddenly, you’re minimising confusion and potential errors. This synergy of technology and hospitality can also give you deeper insights into customer preferences—from popular dishes to typical tipping habits—ultimately helping you craft a dining experience more aligned with your guests’ tastes.

Sustainable success in the food business relies on adaptability. Menus evolve, customers discover new dishes to love, and technology is always on the move. The same logic applies to card payment processing. Even if you switch providers now and land a great deal, you need to periodically re-evaluate that contract. Are your needs changing? Are there new regulations on interchange fees? Has the provider introduced any new charges or new features that could change your bottom line (for better or worse)?

Regular check-ins—maybe every 12 to 18 months—will help ensure your setup remains optimal. If you see new payment trends on the horizon, like a rising preference for QR code payments or even digital wallets, ask if your provider can handle those without tacking on extra costs. In short, be proactive rather than letting fees gnaw away at your profits without you even noticing.

Let’s look at a simplified example comparing two providers for a hypothetical UK restaurant that processes £20,000 monthly in card sales. This is only an illustration, but it shows how different fees might affect your bottom line.

| Provider | Provider A (Current) | Provider B (Alternative) |

|---|---|---|

| Transaction Rate | 2.5% | 1.8% |

| Monthly Fixed Fee | £20 | £10 |

| Terminal Rental | £25 | Included |

| Other Fees | £10 (PCIDSS) | £10 (PCIDSS) |

| Total Monthly Cost | £535 | £370 |

If you run similar numbers for your own situation, you might find equally substantial differences. Those saved pounds can be funnelled back into your menu’s quality, staff bonuses, or marketing new dishes. Or perhaps you simply keep it as extra profit—after all, better margins mean a sturdier business overall.

In a competitive marketplace, your success hinges on making sure every facet of your restaurant is both cost-effective and guest-friendly. Payment processing may not be the most exciting topic—especially compared to sampling new seasonal ingredients—but it’s a vital area that can help you run a healthier, more profitable business.

So, is it time to switch providers for better card fees? If you’re seeing signs of high or unpredictable costs, if your hardware or customer service experience is lacking, or if you just suspect there might be a better solution out there, then it might be. Keep an open mind, do your homework, and weigh the pros and cons. Whether you decide to renegotiate or switch, the goal is to ensure your card payments help your restaurant thrive.

It varies by provider, but many UK restaurants can find rates ranging from 1.5% to 2.5%. The exact fee will depend on your transaction volume, average transaction size, and the type of cards you accept.

Yes, watch for early termination charges, new equipment rental fees, and compliance fees (like PCI DSS). Some providers also add surcharge fees for chargebacks or inactive months, so always read the fine print.

Review it at least once every 12 to 18 months. Payment technology and fee structures can change quickly, so regular check-ups help ensure you’re getting the best deal and the latest features.

Most updated providers supply compact card terminals or can integrate with your current POS system. Some offer app-based payment options, like QR codes, which might reduce your need for extensive new hardware.

Implementing a new provider is simpler than you might think. Plan your timing—preferably during quieter periods at your restaurant—overlap your old and new systems briefly, and train your staff on any new interfaces or hardware to ensure a smooth transition.

Drop us your details below and we’ll reach out within the next 24

sunday elevates your business with insightful data, instant feedback and precise analytics.